Airlines and lessors will take delivery of 21,700 aircraft from 2023-2032, with annual totals topping 2,000 starting in 2025 and edging up slightly throughout the remainder of the forecast period, a new Aviation Week Network commercial activity forecast projects.

Combined with an estimated 10,860 retirements, the global fleet is expected to edge past 44,300 commercial aircraft by the end of 2032, climbing at a compound annual growth rate (CAGR) of 3.5% from the year-end 2022 level of 30,000, the forecast revealed.

Annual retirements will edge up from recent historic lows of around 2% of the global fleet total to 3-3.5% by mid-decade, the forecast said. Annual retirements will average just less than 1,100 during the 10-year forecast period, with a projected peak of 1,300 in 2027. The projected mid-decade spike could see the current lack of used serviceable material (USM) and dwindling engines with green time change rapidly, potentially flooding the market with used parts and engines that can help operators delay overhauls.

Narrowbodies will continue to dominate the delivery landscape, accounting for an estimated 78% of the customer handovers during the next 10 years. Widebodies will account for 13%, regional jet aircraft will take 5%, and turboprops, 4%.

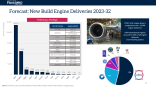

Some 43,400 new engines will be delivered over the next 10 years, the forecast projects—a figure that does not include spares. The CFM Leap family will dominate powerplant deliveries, with 23,500 or 54% of the total.

The aftermarket is expected to grow from $87.6 billion in 2023—a notable jump over 2022—to $112.6 billion in 2032. That reflects a CAGR of 2.8%, a figure that is muted somewhat because of the expected significant jump from 2022 to 2023 due to the recovery’s strength in many markets, which is stimulating demand for aircraft and engine maintenance, repair, and overhaul (MRO) work. While there are still two quarters of financial reporting left in 2022, many MRO providers are projecting year-over-year sales growth levels in the high teens or low 20% range for the full year—a clear sign that the recovery is in full swing.

The global fleet is expected to generate just shy of $1.1 trillion in MRO work in the coming decade. Engine maintenance will be the dominant category, at 46% growing at a 3.1% CAGR throughout the forecast period.

Highlights of the new Aviation Week Commercial Fleet & MRO Forecast were unveiled during an Oct. 6 Aviation Week webinar. The entire forecast is slated to be released in mid-October.

Related Content