CAPA Perspective: The Airline Industry Will Never Be The Same

There is something very important that most airlines either do not recognize or don't wish to: The future airline industry will never be the same again. Vitally, the 2021 industry will, at best, be half the size it was in 2019. Yet the industry is betting the house on a substantial recovery in the 2021 second and third quarters. What's Plan B?

Airlines have enjoyed some tailwinds that helped them remain liquid over the past year, though their debt profiles have deteriorated greatly. These tailwinds included government "generic" economic aid/wage packages, direct equity investments and uniquely low interest rates.

It is surprising how so few airlines went out of business in an unimaginably dreadful year, where international capacity fell to around one-tenth of its previous level and many domestic operations fared only slightly better.

Tipping point ahoy

Government economic support will continue until the second quarter, or maybe longer in the US. But, in the absence of demand, airline income is likely to remain static, while cash burn continues. The vaccine rollout should gradually improve consumer sentiment (in some countries, not all) and the horrific mortality levels should start to subside.

Cash flow is now critical, but we're fast approaching the tipping point. Cash burn cannot continue indefinitely, so airlines will need to become proactive, rather than just "burn the furniture to keep warm."

Cash burn will likely increase when short-haul travelers return because there will be too many seats available. Airlines will seek to defend their market shares, depressing prices. Business travel will remain heavily subdued, hurting yields, and leisure travelers will buy late, making it harder for airlines to accumulate advance cash. Capacity will not stabilize for months and oil prices could surge as broader economic demand rebounds.

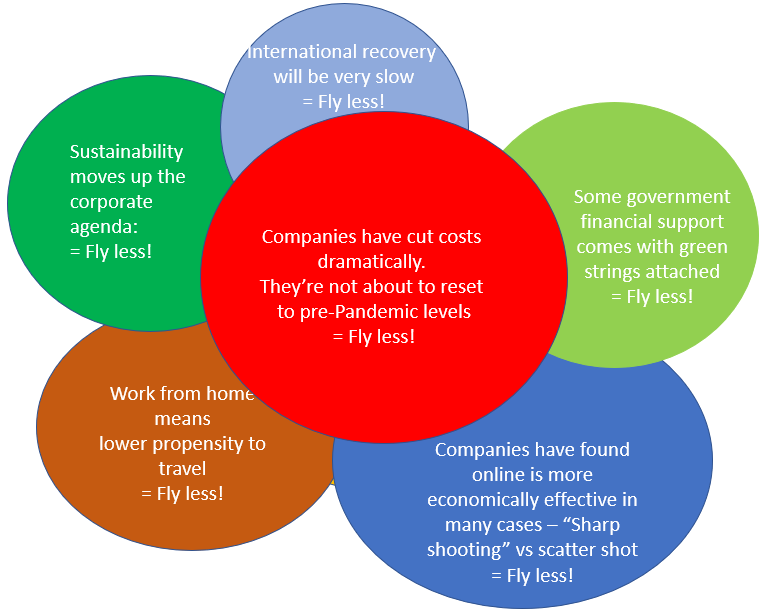

The loss of business travel and added complexity of re-establishing medium- and long-haul international travel will undermine the full-service airline business model.

An unrecognizable industry

The future airline industry will be unrecognizable from its pre-COVID-19 structure, exhibiting the following long list of features:

- Airline revenue streams, already rapidly evolving, will change greatly;

- Passenger and yield profiles will be very different in the short term, pointing to a new trajectory for the medium and longer terms;

- This will be driven by soft consumer demand, diminished business travel and lower average ticket yields;

- The inverse is, necessarily, that ancillaries in one form or another will have to play a much greater role;

- Airlines that have fared better than others over the past year generated 50% or more of their income from non-ticket sources. (They have also been supported in many cases by cargo carriage);

- Other evolving revenue streams include loyalty programs (for Qantas, half of its EBIT within three years); brand leverage and diversification (AirAsia becomes a digital airline, aiming at 50% non-airline revenue by mid-2020s);

- Health and sanitation issues are here to stay;

Internationally it will mean a continuing "hiccup effect" as governments protect their borders from new infections;

- Airlines will incur higher operating costs;

- Airports will need to adapt, expensively, to conform with health needs;

- Standardized testing and recognition of vaccinations will be challenging for years;

- The entire foundation of competition regulation has been undermined;

- Government support for airlines has been so widespread that subsidies will drive much of the near-future growth, especially in international markets;

- This creates fundamental issues around competition and raises the real prospect of the regrowth of protectionism;

- As yield profiles slump, low costs will be even more vital;

- Already, LCCs have expanded market shares across the world;

- Full-service carriers will need to reinvent themselves, including reducing costs;

- Losing business travelers means fewer trunk routes, fewer long-haul services and fewer airlines;

- Higher prices for long-haul international travel.

Reducing total airline revenue by 50% must be transformational; it can mean any or all of the following:

- A much smaller industry, with fewer or smaller airlines (with major implications for creditors and shareholders);

- Bankruptcies or slow painful decline as debt burdens weigh heavily;

- Short haul-where most future growth will come from-becomes much more competitive;

- International travel will be problematic;

- Uncoordinated national responses and the "hiccup effect" of sudden border closures make network planning difficult and costly;

- Long-haul trunk routes, with reduced business travel revenues, will have reduced frequencies and fewer airlines, often subsidized;

- Higher fares for leisure travelers a likely outcome.

- On the sustainability front, pressures will intensify to reduce emissions. This comes with added costs and revenue loss.

The airline industry that finally emerges will be very different from the one that existed before this crisis.